Economic & Market Views

Liquidity leading the way lower?

Today, we offer updates on our economic and financial near-casts, along with our market regime views. As always, we focus on what the economic data tell us about the economy’s current state, what markets tell us about expectations, and our systematic near-casting framework telling us about the near-term. Additionally, we show our Market Regime Portfolio, which applies our understanding of market-implied regimes and portfolio construction to give us a sense of the best exposures in the immediate term. Our observations are as follows:

Growth remains elevated in a downtrend. Our systematic forecasting implies a continuation of this trend into the end of 2021. However, our systems are aligning to suggest a decelerating environment beginning at the end of Q1 2022 extending into Q2 2022.

Inflationary pressures remain stable at high levels. Our systems show a sustained level of inflation across the subcomponents of our Inflation Index and expect high inflation rates through 2021.

Liquidity continues to tighten, setting the stage for a tough 2022. The liquidity transmission mechanism usually leads to a lag between liquidity conditions and market/economic conditions. Our Policy Impulse Index suggests a gloomy outlook for real growth in early 2022, in line with our systematic forecasts for growth.

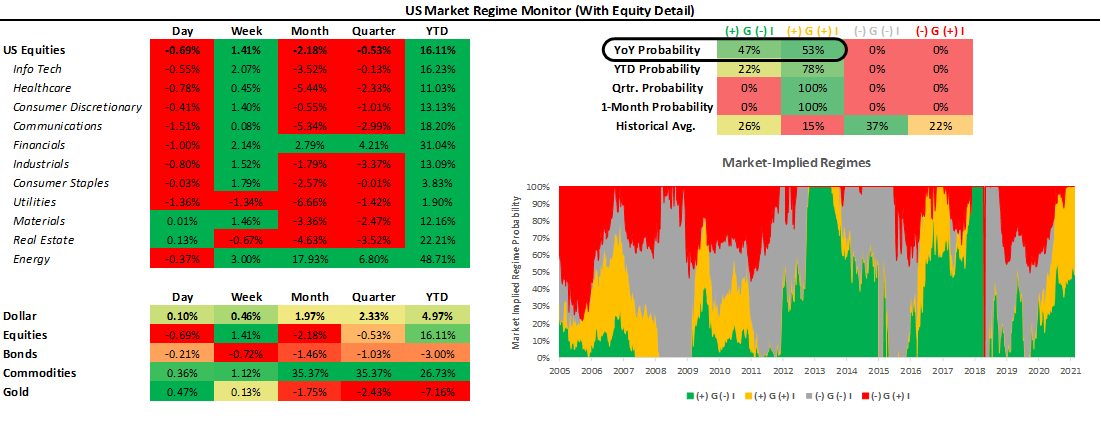

Markets continue to price (+) G (+) I, i.e., rising growth and inflation. After a brief period of transitioning to (+) G (-) I, markets have returned to (+) G (+) I, reflecting the strong relative performance of the commodity complex. What remains clear is that we remain very much in a market environment conducive to rising growth exposures, despite the back-and-forth between rising and falling inflation pricing.

The future is dynamic, and our systems adjust as new information is available. Our bias is to allocate for the existing regime while trying to peek around the corner to what the future may hold. Our Market Regime Portfolio aims to capture the current macroeconomic trend, and our systematic forecasts serve as our way of estimating what the next trend is likely to be. After a negative performance in September, the Market Regime Portfolio is up this month due to a rebound in risk assets— down 2% in September but up 3% thus far this month, taking the cumulative performance to approximately 24% this year. Our Market Regime signal shifted in the week ending on October 8th to reflect the change to (+) G (+) I from (+) G (-) I as the dominant trend, i.e., preferring commodities. We designed our system to be aggressive, wholly allocating to the current Market Regime, and a more balanced approach would likely spread bets a little wider. From a discretionary perspective- given the nearly tied odds between (+) G (+) I and (+) G (-) I, we think it is worth considering a bias towards rising growth assets but to remain less aggressive on inflation tilts.

However, our systems are increasingly aligning to signal a challenging environment for risk assets in Q1-Q2 2022. We discuss all this and more in the pages that follow.

Economic Growth: Trending Lower

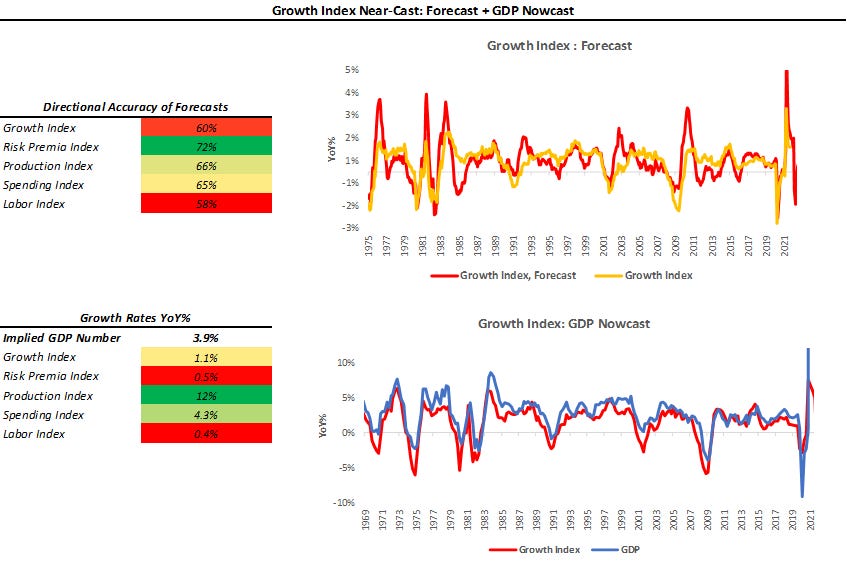

Our Growth Index is our high-frequency measure of the growth impulse to GDP from a wide range of comprehensive economic data. The Growth Index has four subcomponents: risk premia, spending, production, and labor markets. The index measures economic activity at a higher frequency (monthly) and lower latency than quarterly GDP. Current economic data, which feeds the Growth Index, is currently pointing to 3.9% real GDP growth:

As we can see above, the Growth Index estimates real GDP growth in real-time. The Growth Index has a directional accuracy of 88% in nowcasting real GDP growth. More importantly, unlike many regression-fitted estimates, our Growth Index has greater accuracy in nowcasting GDP downturns- our downside directional accuracy is 95%. When we think about our Growth Index, we prefer to focus not on the estimated magnitude of the nowcast but rather the acceleration or deceleration of the nowcast. As we can see above, our Growth Index implies GDP growth of 3.9% on a year-over-year basis, a modest increase since our last publication, where it was at 3.8%. Additionally, we can break parts of the Growth Index into Sub-Indexes to show the distribution of economic forces:

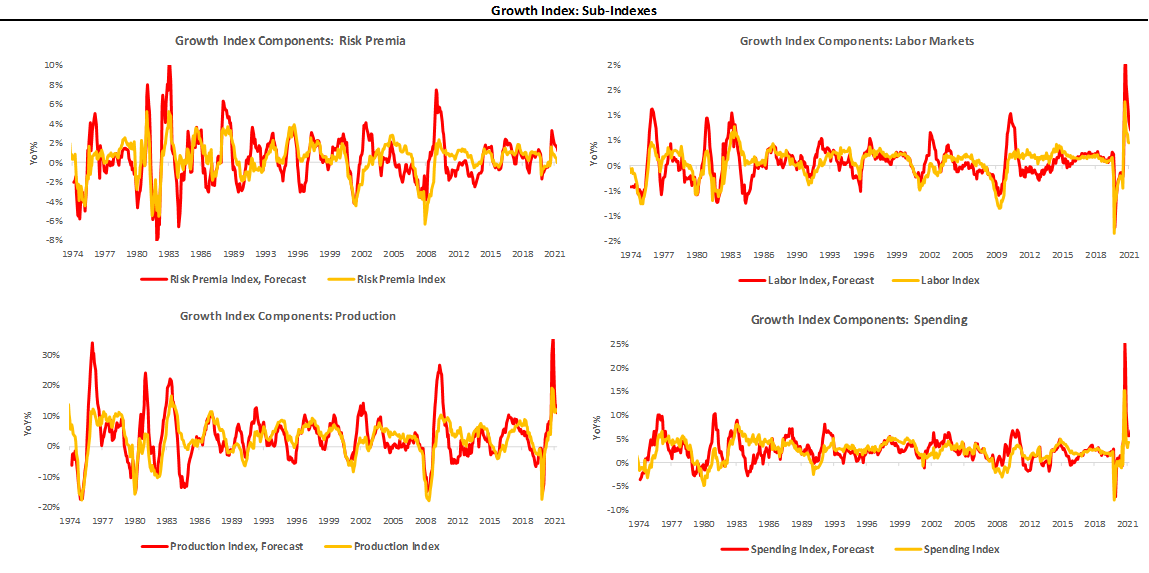

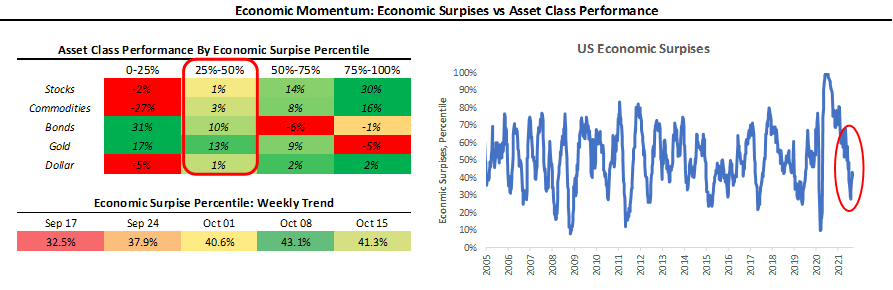

As we can see above, growth remains broad-based and elevated but continues to trend lower as our systems expected. Since our last publication, the sustained elevation of economic growth rates has ameliorated the decline in economic data surprises:

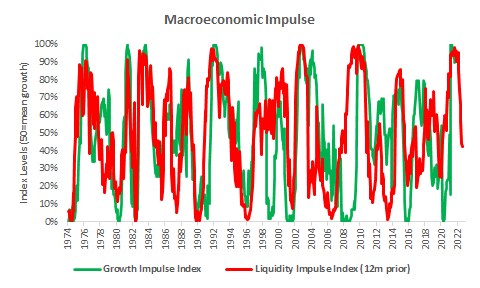

With the latest reading at 41.3%, realized economic data relative to expectations are sufficiently far from the lowest quartile of economic surprises, where the distribution of returns for risky assets becomes more negative. However, as we have mentioned previously, we are increasingly likely to end up there in Q1-Q2 2022. This move, if realized, will likely be driven by declining liquidity. The liquidity transmission mechanism takes several months to a year to find its way into real economic data. Therefore, we expect the deteriorating liquidity impulse (which we have documented here consistently) to find its way into deteriorating economic conditions in 2022. We show how this has borne out over past cycles below:

Above, we show our Policy Liquidity Impulse Index 12 months ago versus our Growth Impulse Index. As we can see, while there have been variations in cycle-time, moves in significant changes in liquidity typically tend to result in changes in subsequent economic activity. Note: The Growth Impulse Index is our Growth Index 2.0, more to come on this soon.

Inflation: Still Elevated

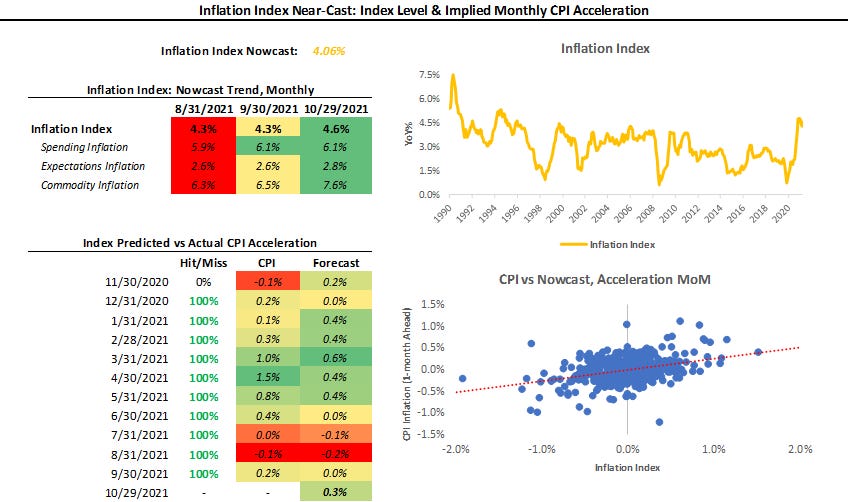

Our Inflation Index is our high-frequency measure of the impulse to inflation from a wide range of comprehensive inflation data. Our Index Index aggregates data across measures of Spending, Expectations, and Commodities to give us an understanding of the degree and pervasiveness of inflation. Further, our Inflation Index allows us to nowcast inflation on an ongoing basis, giving us some insight into upcoming CPI prints:

Our Inflation Index currently sits at 4.06%, an acceleration from our last publication, when it was at 3.89%. This acceleration has been reflected in the intervening CPI prints, which have shown modest acceleration on a month-over-month basis. Our Inflation Index has been 58% accurate in determining the acceleration or deceleration of the following print in CPI since 1980. Over the last 12 months, the Inflation Index has had a 92% accuracy in estimating the monthly acceleration in CPI. Given the recent accuracy of the Inflation Index, we take a considerable signal from its further strengthening since our last publication. To complement the immediate-term view provided by the Inflation Index, we also offer our systematic CPI forecast to estimate the future cyclical trend in inflation:

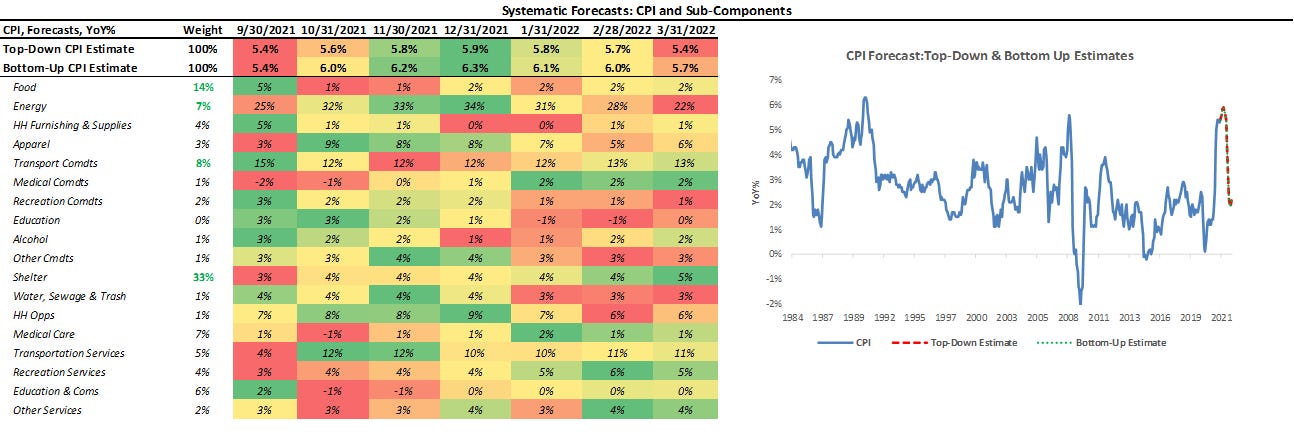

Above, we show our systematic forecasts of CPI and its subcomponents. We include both a top-down estimate and a bottom-up estimate- obtained via forecasting each subcomponent. There has been (and continues to be) a debate on the underlying nature of inflation- i.e., whether the current strength in inflation is transitory. A significant component of this debate is the underlying secular dynamics that modulate inflationary pressures and underly cyclical moves in inflation. The question before us today is whether these secular dynamics have been altered in a way that changes the underlying inflationary trend to one that is higher than the pre-pandemic trend. At this junction, we are still building the machinery to evaluate these underlying trends quantitatively; therefore, we remain hesitant to express views on the subject. However, from an empirical perspective, it is clear that the underlying trend has shifted higher. Therefore, we think it prudent to assess and evaluate inflation on a print-by-print cyclical basis.

Liquidity: Leading The Way lower?

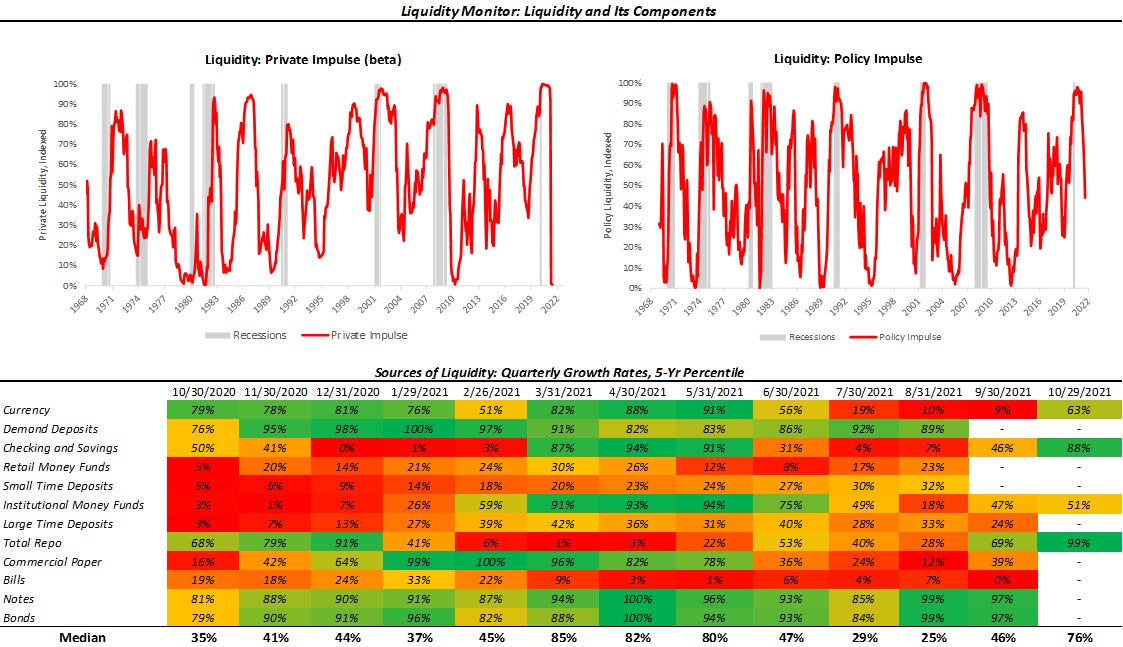

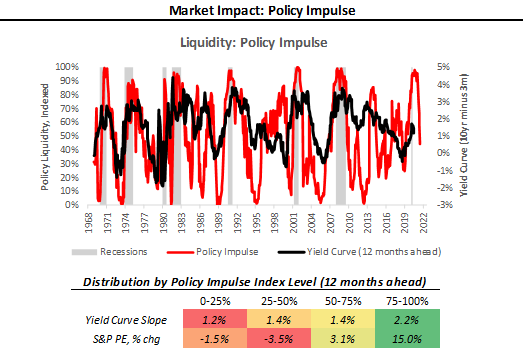

As part of our analytical framework, we assess the health of the countries’ income statement via growth and inflation and the health of its balance sheet via liquidity. Below, we show our Liquidity Monitor, where we offer our measures of the Liquidity Impulse coming from policy & the Private sector. Additionally, we provide the normalized growth of some of the major subcomponents in the heatmap: (please note our Private Impulse is a beta version)

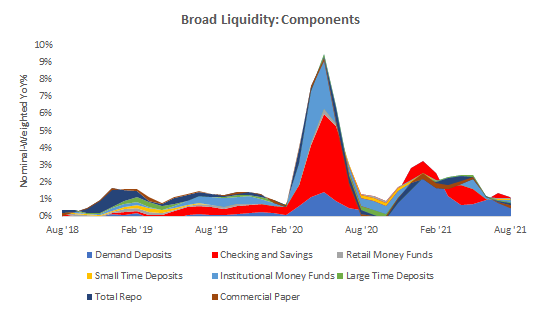

As we have highlighted in the past, while the liquidity complex isn’t contracting, the liquidity impulse is fading. For further context, we show the simple-sum measures of the table above:

As we can see above, demand deposits have been the most significant nominal contributor to the private liquidity complex in 2021, coming off the back of essentially joint monetary-fiscal programs in response to COVID-19. Looking ahead, with direct fiscal transfers less likely, the impulse for these significant increases in private sector cash balances is expected to continue to reduce significantly. Recall, liquidity shocks potentiate economic and market shocks. Therefore, as liquidity dries, the potential for economic growth above or at its cycle trend decreases. Furthermore, the reduction deterioration of the liquidity impulse doesn’t bode well for risky assets, and creates a higher demand for high-quality, pristine assets, i.e., flattens yield curves:

The Policy Impulse Index typically rises to precede steepening yield curves and richening valuations. This is because the Policy Impulse Index measures pristine liquidity coming from monetary and fiscal authorities, which form the base of capital that can migrate to risk-taking and economic growth. Today, the slowdown in liquidity growth essentially reduces the “dry powder” available for the same process in the future. Therefore, the reduction in liquidity will eventually find its way into the financial assets and the economy, but likely with a lag. In addition to the fading of fiscal injections, the gradual reduction in net purchases by the Federal Reserve will dampen the liquidity environment. With a shortage of Treasury bills and a strong demand for safe assets, a tightening of monetary conditions will likely result in increased demand at the long end of the curve, consistent with our systematic forecasting of the market regime. These moves are not imminent, but as always, we try to keep you ahead of the next significant change to the environment.

Market-Implied Regime: (+) G

Using the performance of various asset classes, we can extract what markets are implying which particular economic regime we are experiencing. Below, we show what markets are telling us about the current growth and inflation regime:

As we have mentioned before, we can be in one of four regimes:

(+) G (-) I: Rising Growth, Falling Inflation

(+) G (+) I: Rising Growth, Rising Inflation

(-) G (+) I: Falling Growth, Rising Inflation

(-) G (-) I: Falling Growth, Falling Inflation

Using our understanding of asset markets, we can classify periods into one of the four regimes mentioned above. Further, we can use the regime obtained from our market-implied odds with trend-following and cross-sectional momentum measures to create portfolio signals. To provide maximum accessibility, we truncate the portfolio construction into three stages:

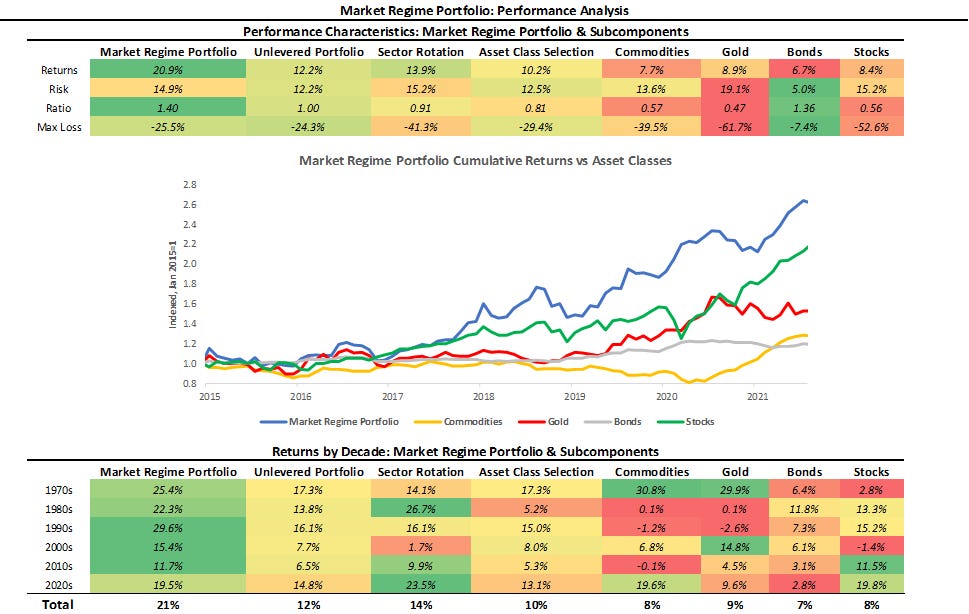

Asset Class Selection: We create a portfolio that selects asset class exposure based on the current market-implied regime.

Sector Rotation: We create an equity rotation portfolio that chooses sectors based on their market-regime preference- to avoid overfitting, we choose these logically rather than based on our historical regime performance.

Unlevered Portfolio: We combine Asset Class Selection and Sector Rotation.

Market Regime Portfolio: Finally, we create our Market Regime Portfolio by ex-ante targeting equity volatility, i.e., we use leverage to match equity volatility.

Below, we show the results of this process versus major asset classes. Additionally, we show the performance characteristics over the decades since the 1970s:

As we can see above, our systematic Market Regime Portfolio has a strong performance across measures and is consistent over time. The portfolio is designed to be decisive and aggressive, wholly allocating to assets that prefer the current regime, with no diversifying exposures. We take a significant signal from our Market Regime Portfolio, which has now confirmed a (+) G (+) I environment, i.e., one that predominantly prefers commodities. However, given the closely contested battle between (+) G (+) I and (+) G (-) I, the signal has switched back-and-forth over the last few weeks. From a discretionary perspective, we think it is prudent for those using our signals to consider spreading their bets when it comes to the inflation bias of their trades but remain strongly tilted towards a growth bias.

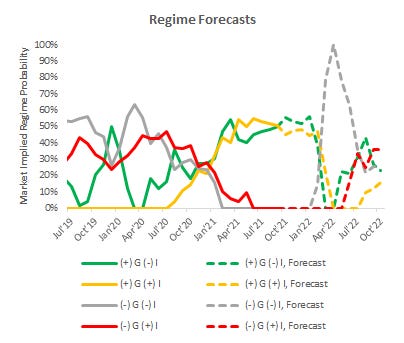

Our systematic forecasts attempt to peer around the corner into the next regime and currently tell us two things. First, we are likely to see a closely contested (+) G environment in the immediate. Second, the next likely regime will be (-) G (-) I, which would be consistent with our fundamental forecasts and our leading liquidity aggregates:

This regime change coincides with the timing of liquidity reduction from the Federal Reserve, alongside a potential deterioration in economic growth. Therefore, as we get closer, we grow more vigilant. To help us deal with the risks of this possible change, we will be launching several trend monitors, which we are excited to share with you soon.

Conclusions:

To reiterate the signals coming from our systems:

Growth remains elevated in a downtrend, and our systematic forecasts indicate the brunt of the declaration will occur in Q1-Q2 of 2022.

Inflationary pressures remain stable at high levels. The empirical trend in inflation has moved upwards, and only time will tell if this trend just outsized cyclicality. We think managing inflation risk on a print-by-print basis is optimal.

Liquidity is leading the way lower. Fading fiscal impulse, tightening monetary policy, and slowing credit creation bode for a tighter liquidity environment in 2022, i.e., flatter curves and cheaper valuations.

Markets continue to price (+) G, rising growth. While there may be some back and forth about the inflationary nature of this rising growth environment, we remain in an environment that favors risk.

Overall, the environment still looks positive for risk and (+) G exposures. However, declining liquidity reduces the future potential for both market moves and economic expansion. While the rest of 2021 looks to continue to have a positive backdrop, conditions continue to align for a tough H1 2022. For the time being, our systems continue to think risk remains well supported by elevated growth rates. We are getting closer to a regime change, and we will keep you updated on the evolution of our systematic outlook. Until next time.