Economic & Market Views

Omicron?

Today, we offer updates on our economic and financial near-casts, along with our market regime views. As always, we focus on what the economic data tell us about the economy’s current state, what markets tell us about expectations, and our systematic near-casting framework telling us about the near-term. Additionally, we show our Market Regime Portfolio, which applies our understanding of market-implied regimes and portfolio construction to give us a sense of the best exposures in the immediate term. Finally, we have received numerous inquiries regarding the Omicron variant and its impact on the US economy and markets. Therefore, we thought it essential to bring you our updated models and monitors. Our systems steered us well through the initial outbreak of COVID-19, and consequently, we remain confident they are robust enough to manage the risk surrounding variants. Given the topical nature of this note, we primarily provide model updates, and commentary updates will be limited to our summary & conclusions. Our observations are as follows:

Economic growth remains elevated. Our systematic near-casting of US economic growth puts US growth at approximately 3.6%, slightly higher than our last publication. Our systematic forecasts imply elevated growth relative to its cycle mean in December.

Inflation is still high. Our comprehensive inflation measures continue to signal that inflation has stabilized at a high level, albeit moderating minimally. Our systematic forecasts imply elevated inflation relative to its cycle mean in December.

Liquidity conditions are officially tighter. With the Fed tapering asset purchases, the policy impulse is going to deteriorate considerably. The question before markets is whether a combination of organic demand (fueling private cash balances) and market finance (fueling asset purchases) can fill the hole. It is a tall order.

Markets are pricing (+) G, i.e., rising growth. Over the last month, there has been a rise in risk-off and inflationary pricing, but the underlying trend remains supportive of rising growth. We would need sustained moves like last week to catalyze a regime shift. Furthermore, markets have reacted strongly to the threat of the Omicron variant. While a future outbreak might cause a regime change, our systems tell us it is simply too early to make any conclusive assessment.

The future is dynamic, and our systems adjust as new information is available. Our bias is to allocate for the existing regime while trying to peek around the corner to what the future may hold. Our Market Regime Portfolio aims to capture the current macroeconomic trend, and our systematic forecasts serve as our way of estimating what the next trend is likely to be. Much like the broad equity market, our Market Regime Portfolio— which is aggressively allocated to equities— took a hit, taking cumulative performance for 2021 to 26%. However, our combined tilts towards Tech, Consumer Discretionary, & Real Estate have outperformed on a relative basis, eking out positive performance. Our systems continue to indicate that rising growth exposures are likely to perform well.

In assessing the threat of a vaccine-resistant strain of COVID-19, we think the best historical analog is the initial outbreak of the COVID-19 virus in 2020. Our systems were able to steer us well through this period, and we would expect a similar outcome in the event of a significant risk-off. Currently, our Market Regime Signals do not indicate a regime change, though short-term market pricing has had a risk-off hue. Furthermore, our Momentum Monitor doesn’t show trend persistence in risk-off assets at this juncture. Overall, our systems tell us that it is simply too early to make any major changes to the outlook.

Economic Growth: Still Strong

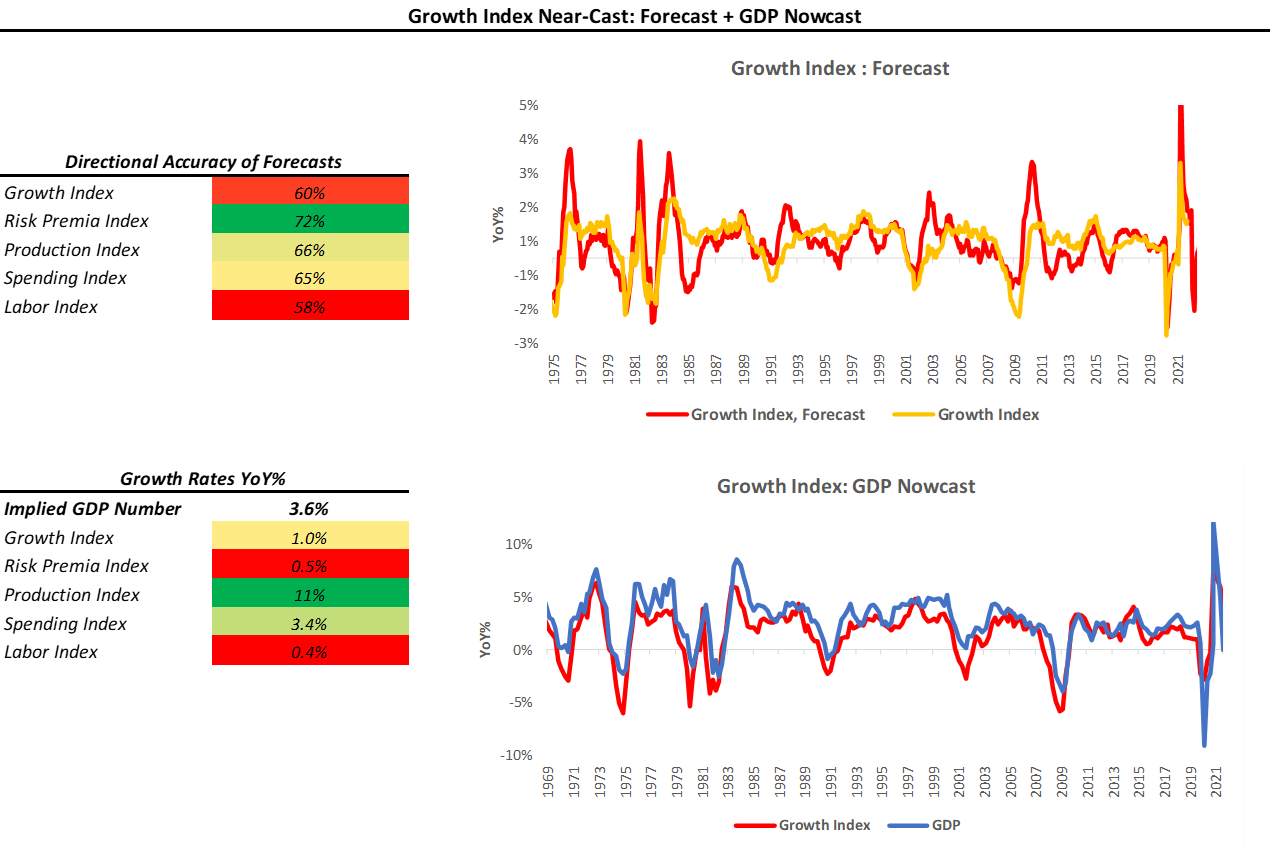

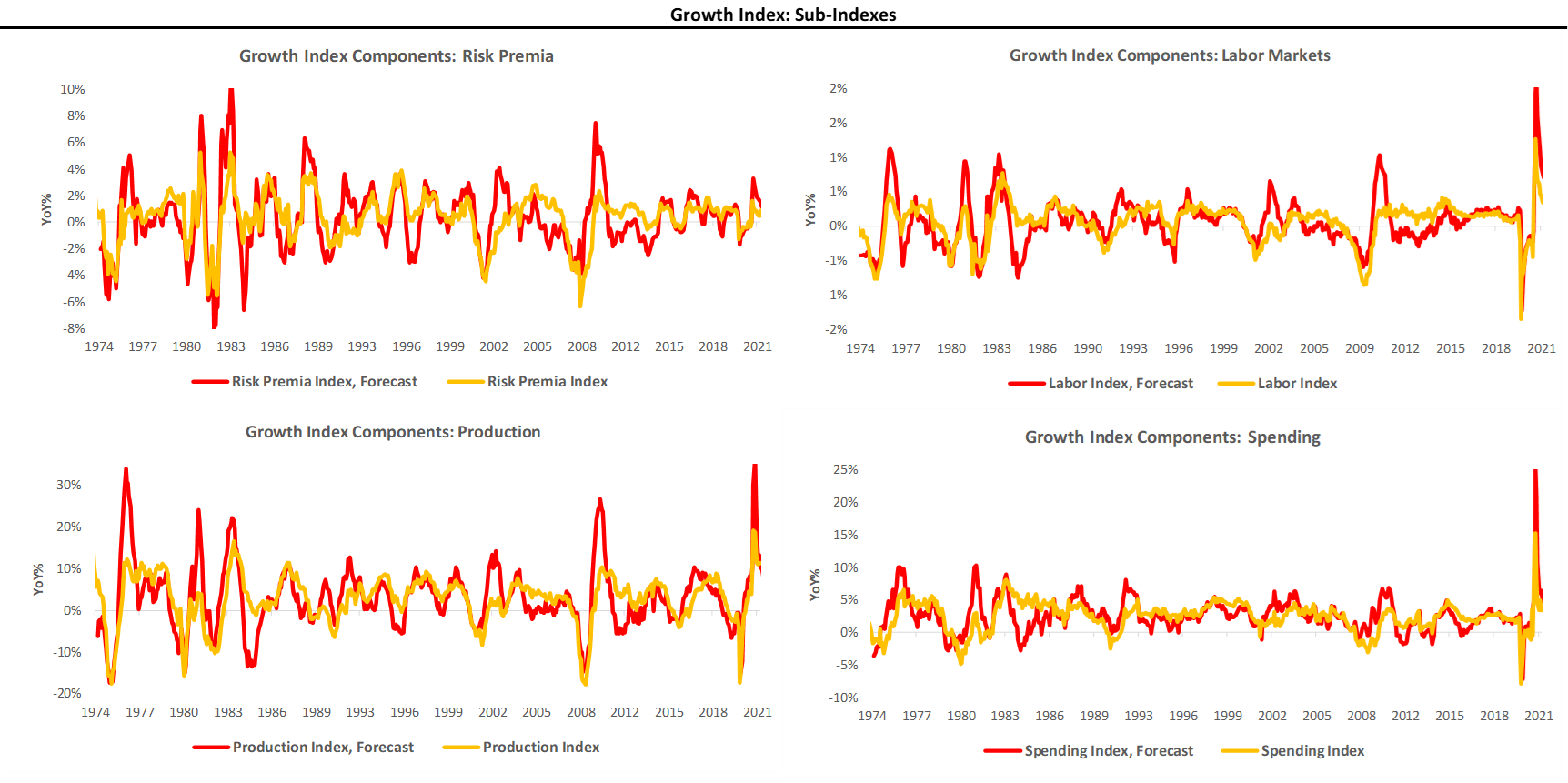

Our Growth Index is our high-frequency measure of the growth impulse to GDP from a wide range of comprehensive economic data. The Growth Index has four subcomponents: risk premia, spending, production, and labor markets. The index measures economic activity at a higher frequency (monthly) and lower latency than quarterly GDP. Current economic data, which feeds the Growth Index, is currently pointing to 3.6% real GDP growth:

As we can see above, the Growth Index estimates real GDP growth in real-time. The Growth Index has a directional accuracy of 88% in nowcasting real GDP growth. More importantly, unlike many regression-fitted estimates, our Growth Index has greater accuracy in nowcasting GDP downturns- our downside directional accuracy is 95%. When we think about our Growth Index, we prefer to focus not on the estimated magnitude of the nowcast but rather the acceleration or deceleration of the nowcast. As we can see above, our Growth Index implies a GDP growth of 3.6% year-over-year, an increase since our last publication, at 3.5%. Additionally, we can break parts of the Growth Index into Sub-Indexes to show the distribution of economic forces:

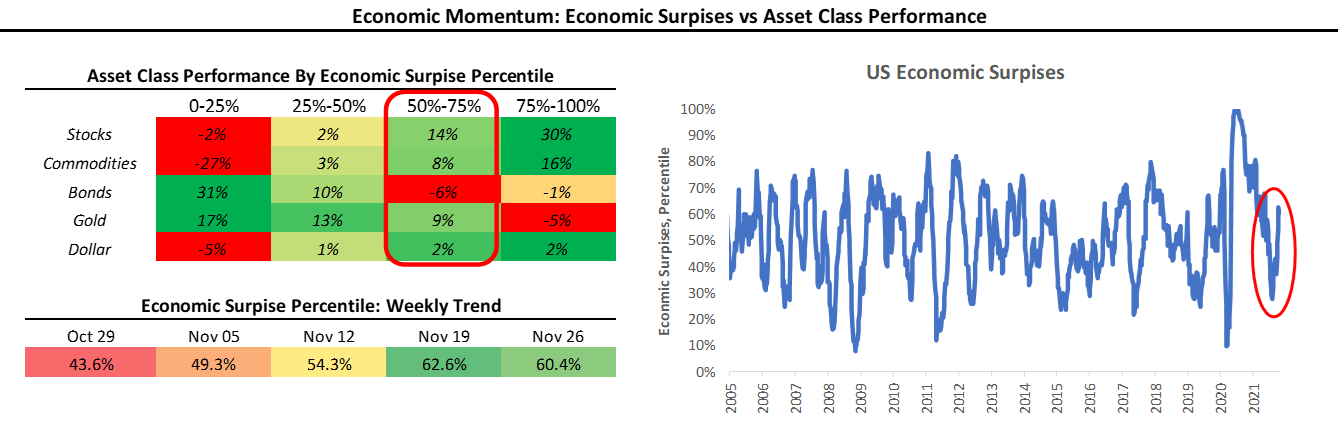

As we can see above, while economic growth does seem to be trending lower, there has been a slowing of the deceleration. The combination of all this data has led to an environment where economic surprises are still above their historical mean:

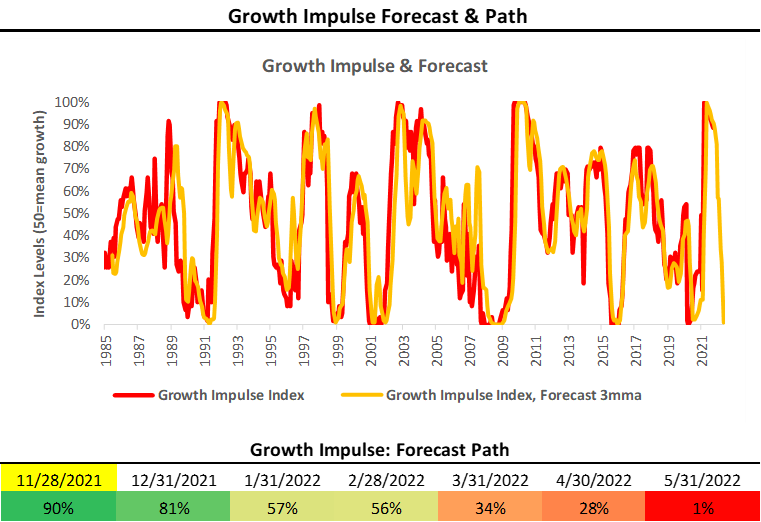

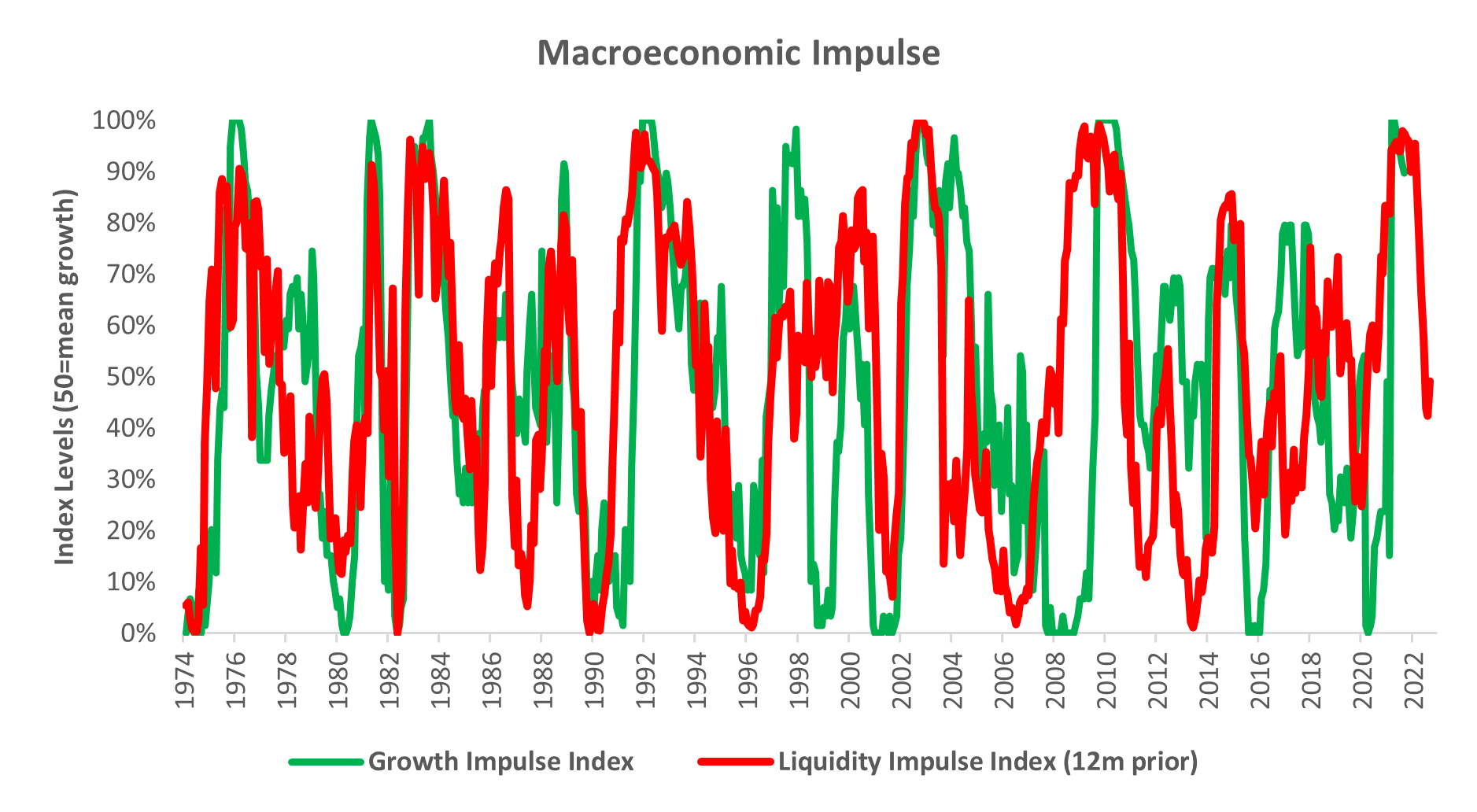

With the latest reading at 60.4%, realized economic data relative to expectations are in the second-highest historical quartile, an environment in which equities and commodities thrive and bonds are weak. Finally, we show our systematic forecasts for our Growth Impulse Index. A value above 50% indicate economic growth above the current cycle mean, and values below 50% indicate economic growth below the cycle mean:

This forecasted slowdown in growth is confirmed by the decline in our Policy Liquidity Index, which typically leads economic activity by 6-12 months. Therefore, while we think the current market environment remains well-supported by elevated growth rates, there is increasingly less room for this to run.

Inflation: Still Elevated

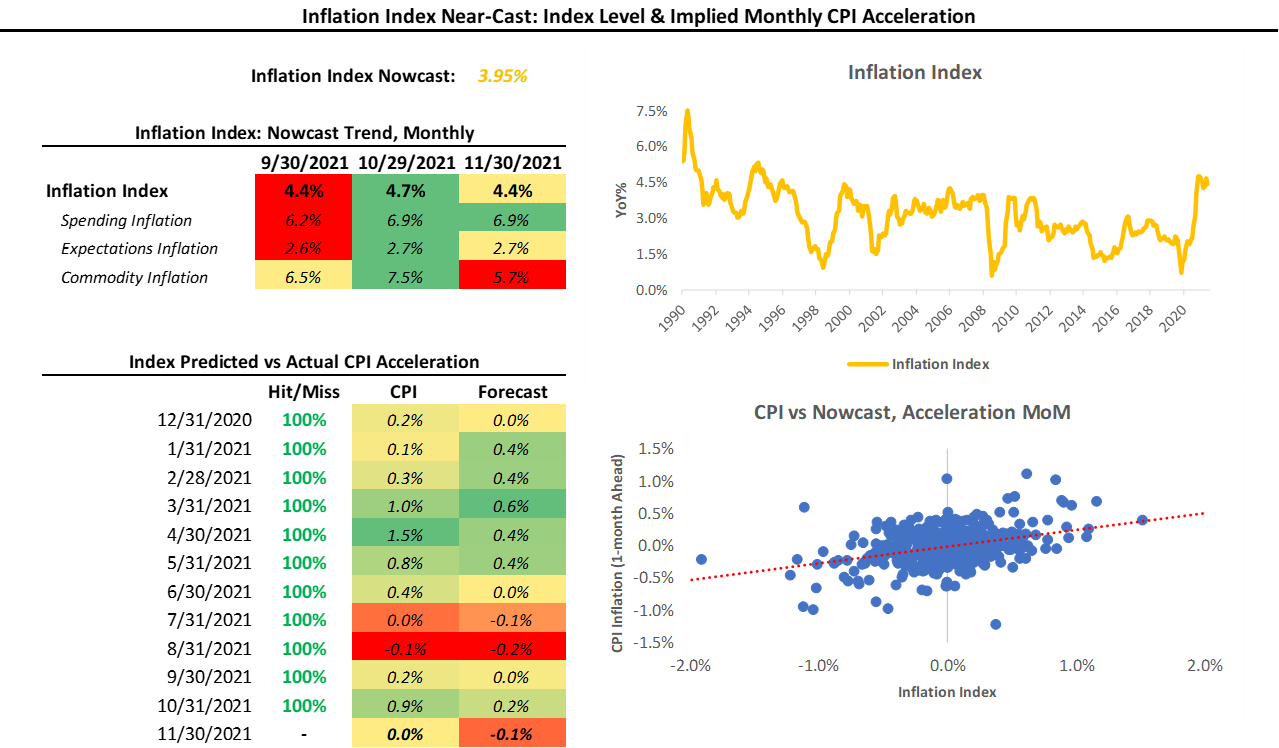

Our Inflation Index is our high-frequency measure of the impulse to inflation from a wide range of comprehensive inflation data. Our Index Index aggregates data across measures of Spending, Expectations, and Commodities to give us an understanding of the degree and pervasiveness of inflation. Further, our Inflation Index allows us to nowcast inflation on an ongoing basis, giving us some insight into upcoming CPI prints:

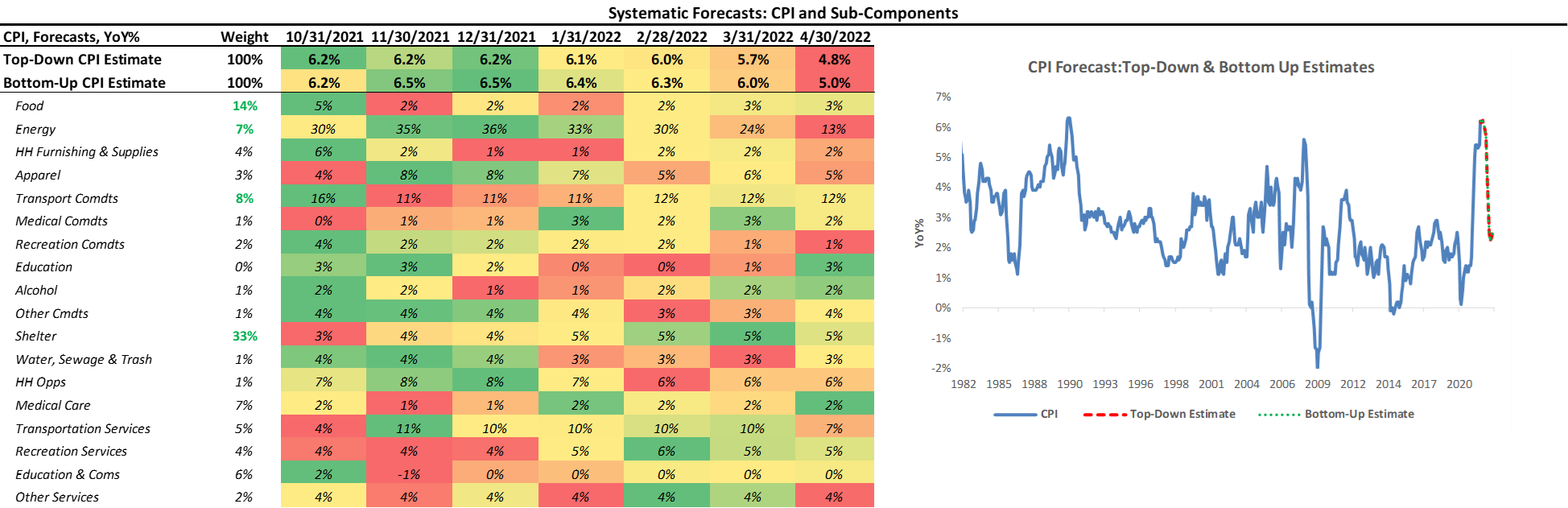

Our Inflation Index currently sits at 3.95%, marginally lower since our last publication at 4.02%. Our Inflation Index has been 58% accurate in determining the acceleration or deceleration of the following print in CPI since 1980. Over the previous 12 months, the Inflation Index has had a 92% accuracy in estimating the monthly acceleration in CPI. Given the recent accuracy of the Inflation Index, we take a considerable signal from its recent stabilization at higher levels. To complement the immediate-term view provided by the Inflation Index, we also offer our bottom-up systematic CPI forecast to estimate the future cyclical trend in inflation:

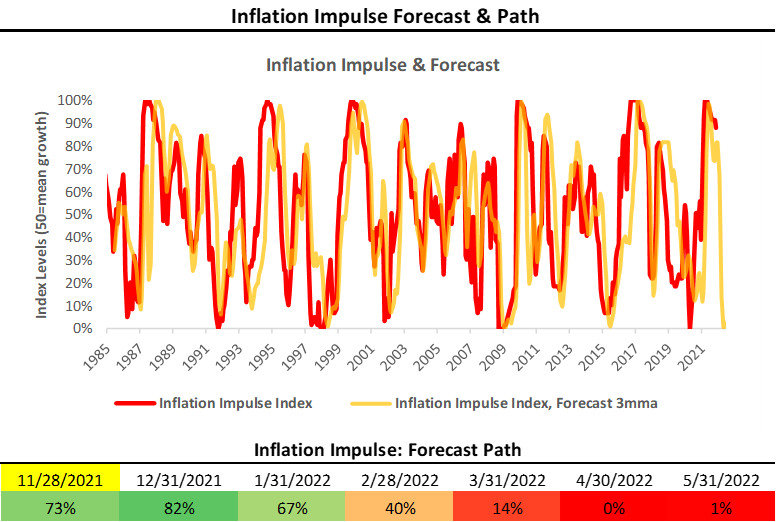

Finally, we show our systematic forecasts for our Inflation Impulse Index. A value above 50% indicate inflationary pressures above the current cycle mean, and values below 50% indicate inflationary pressures below the cycle mean:

With regards to managing inflation risk, we reiterate:

“There has been (and continues to be) a debate on the underlying nature of inflation- i.e., whether the current strength in inflation is transitory. A significant component of this debate is the underlying secular dynamics that modulate inflationary pressures and underly cyclical moves in inflation. The question before us today is whether these secular dynamics have been altered in a way that changes the underlying inflationary trend to one that is higher than the pre-pandemic trend. We are still building the machinery to evaluate these underlying trends quantitatively; therefore, we remain hesitant to express views on the subject. However, from an empirical perspective, it is clear that the underlying trend has shifted higher. Therefore, we think it prudent to assess and evaluate inflation on a print-by-print cyclical basis.”

Our view remains that this is the optimal approach during an environment with a highly uncertain inflation outlook. Therefore, we will continue to monitor changes in inflation dynamics closely.

Liquidity: Can The Private Sector Fill The Hole?

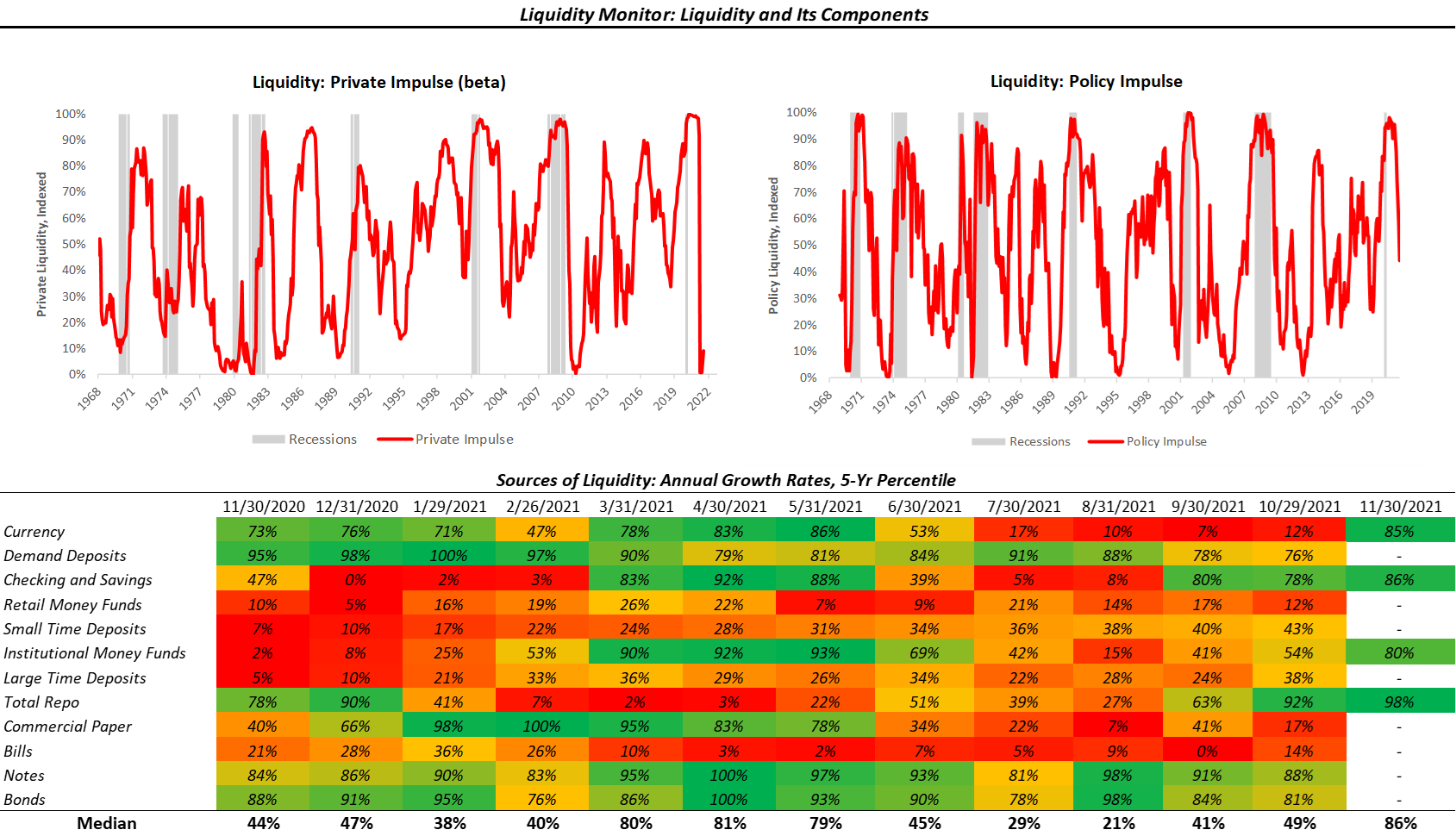

As part of our analytical framework, we assess the health of the countries’ income statement via growth and inflation and the health of its balance sheet via liquidity. Below, we show our Liquidity Monitor, where we offer our measures of the Liquidity Impulse coming from policy & the private sector. Additionally, we provide the normalized growth of some of the major subcomponents in the heatmap: (please note our Private Impulse is a beta version)

To offer further insight into the liquidity environment, we show some simply-sum measures of the aggregates above. For ease of reading, we show some of the simple-sum components of liquidity, grouped into Real Economy, Market Finance, and Government Finance:

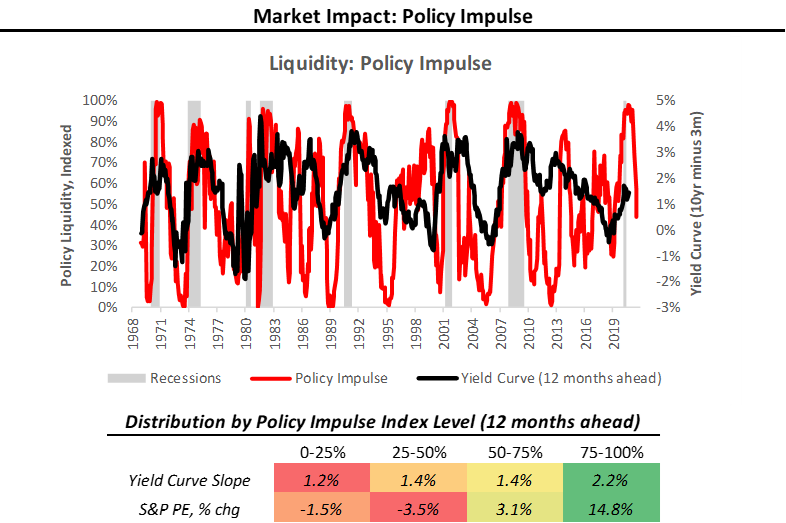

Above, we see that private sector liquidity, both in the real economy and market finance, continues to expand. The question with regards to the liquidity outlook is two-fold. First, can the private sector organically increase cash balances to replace the impulse from fiscal programs? Second, can private sector market finance (repo, commercial paper, shadow banks) fill the hole created by the slow withdrawal of QE? Summarily, we think these are both tall orders and unlikely. Fortunately, the leading nature of liquidity precludes us from the need to forecast these variables. Further, our Policy Impulse Index has already turned lower, telling us that liquidity-based support for the economic expansion is already fading:

Additionally, as liquidity fades and economic growth (potentially) declines, the demand for high-quality assets and collateral rises, i.e., US bonds are increasingly in demand:

The Policy Impulse Index typically rises to precede steepening yield curves and richening valuations. This relationship is because the Policy Impulse Index measures pristine liquidity coming from monetary and fiscal authorities, which form the capital base that can migrate to risk-taking and economic growth. Today, the slowdown in liquidity growth essentially reduces the “dry powder” available for the same process in the future. Therefore, the reduction in liquidity will eventually find its way into the financial assets and the economy, but likely with a lag. In this environment, growth slows, valuations tighten, and bonds are relatively attractive. We expect these dynamics to drive the next regime change, which aptly brings us to our next section.

Market-Implied Regime: (+) G

Using the performance of various asset classes, we can extract what markets are implying which particular economic regime we are experiencing. Below, we show what markets are telling us about the current growth and inflation regime:

As we have mentioned before, we can be in one of four regimes:

(+) G (-) I: Rising Growth, Falling Inflation

(+) G (+) I: Rising Growth, Rising Inflation

(-) G (+) I: Falling Growth, Rising Inflation

(-) G (-) I: Falling Growth, Falling Inflation

Using our understanding of asset markets, we can classify periods into one of the four regimes mentioned above. Further, we can use the regime obtained from our market-implied odds with trend-following and cross-sectional momentum measures to create portfolio signals. To provide maximum accessibility, we truncate the portfolio construction into three stages:

Asset Class Selection: We create a portfolio that selects asset class exposure based on the current market-implied regime.

Sector Rotation: We create an equity rotation portfolio that chooses sectors based on their market-regime preference- to avoid overfitting, we choose these logically rather than based on our historical regime performance.

Unlevered Portfolio: We combine Asset Class Selection and Sector Rotation.

Market Regime Portfolio: Finally, we create our Market Regime Portfolio by ex-ante targeting equity volatility, i.e., we use leverage to match equity volatility.

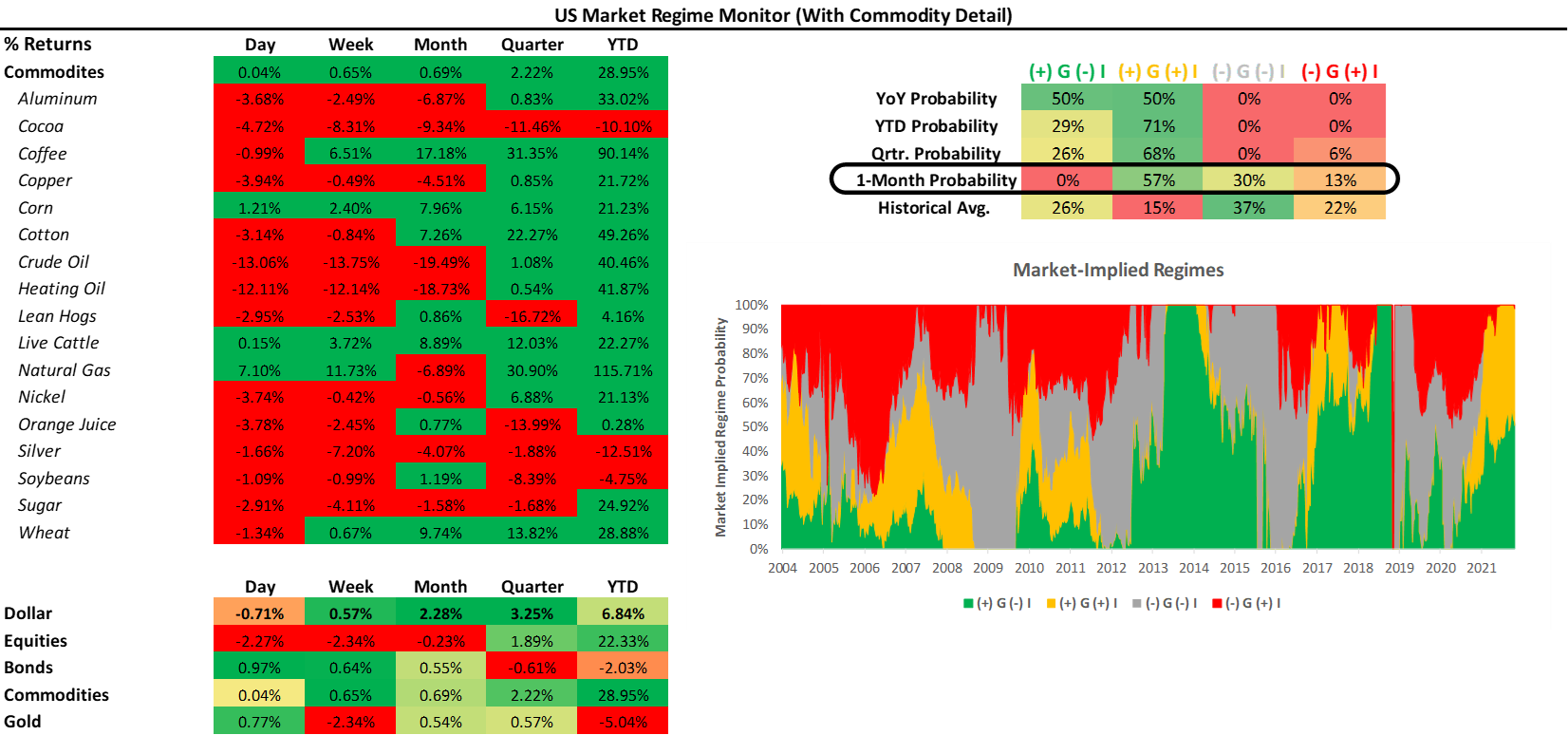

Below, we show the results of this process versus major asset classes. Additionally, we offer the performance characteristics over the decades since the 1970s:

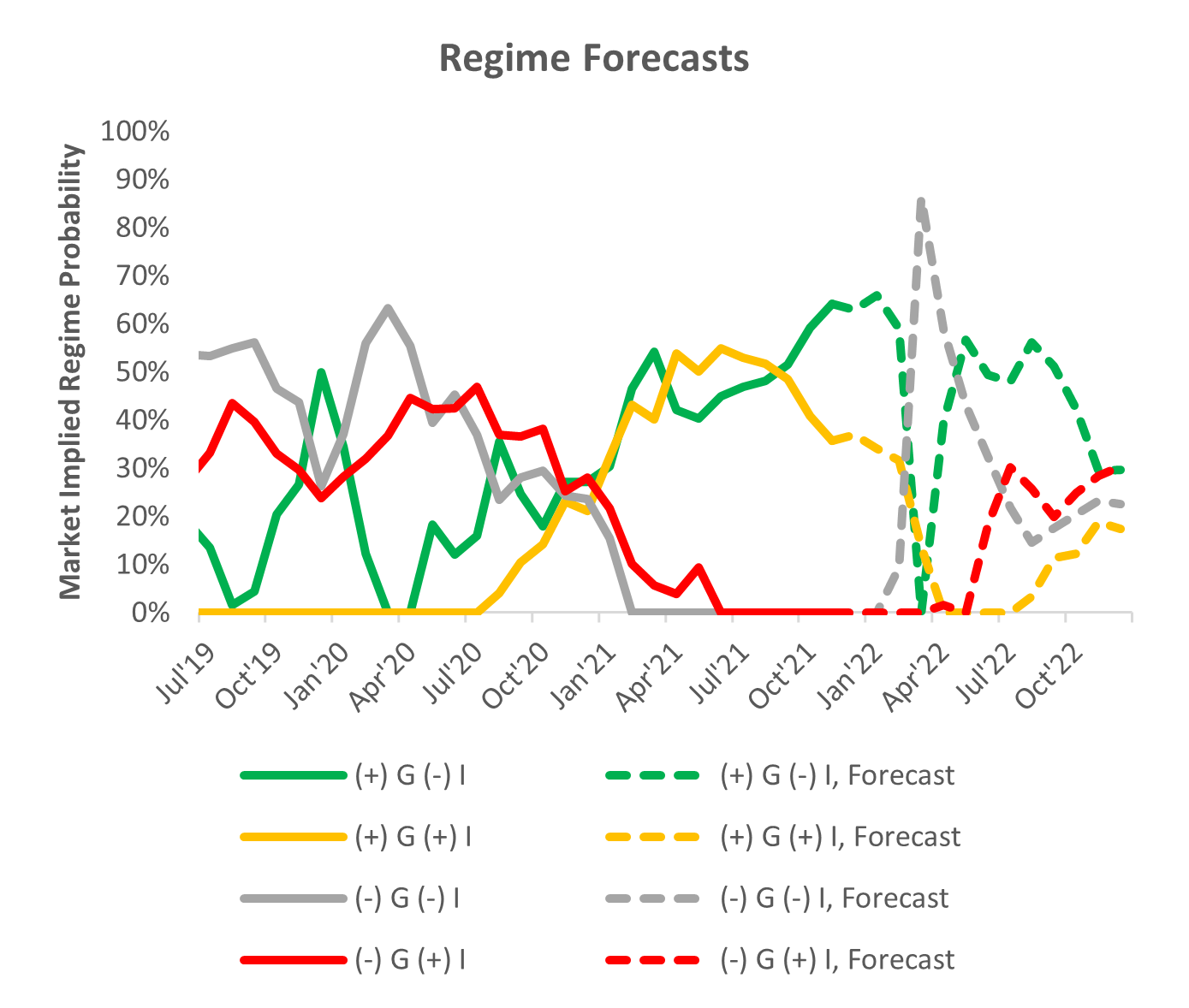

As we can see above, our systematic Market Regime Portfolio has a strong performance across measures and is consistent over time. The portfolio is designed to be decisive and aggressive, wholly allocating to assets that prefer the current regime, with no diversifying exposures. While our Market Regime Signal helps us understand the current market trend, our systematic forecasts attempt to peer around the corner into the next regime:

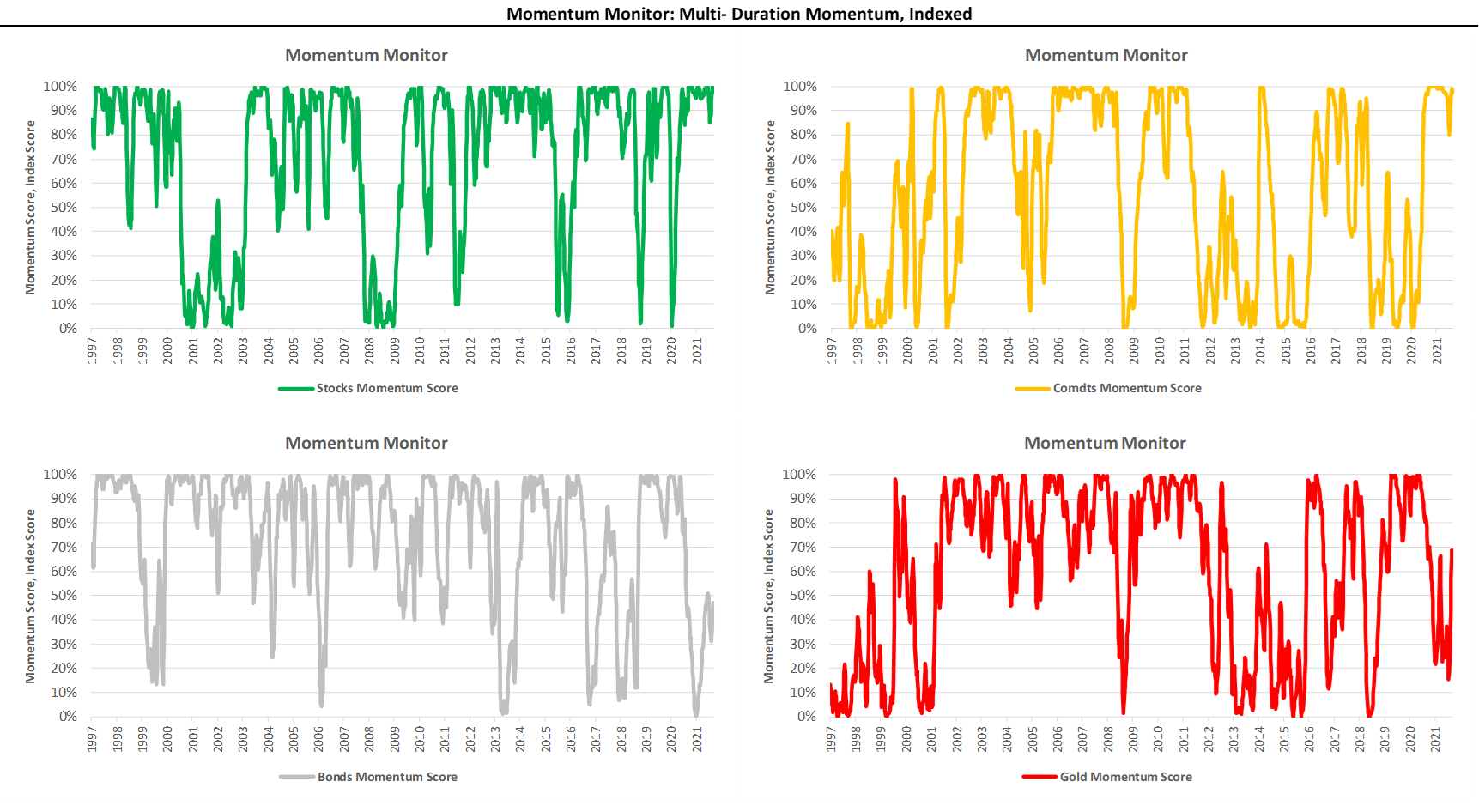

To augment the timeliness of these moves, we also show our Momentum Monitor at the asset class level. Our Momentum Monitor uses a multi-durational approach to momentum, allowing us to better assess changes within our Market Regimes. A value above 50% indicates upside momentum, whereas a value below 50% indicates downside momentum:

As we can see above, our Momentum Monitors for both Stocks and Commodities remain elevated, while the same measures for bonds and commodities remain depressed. We would need to see a significant reversal of these dynamics to precede a regime change.

Conclusions:

To reiterate the signals coming from our systems:

Economic growth remains elevated.

Inflation is stable at high levels.

Liquidity conditions have tightened and will likely impact the economy & markets in 2022.

Markets have favored rising inflation this month, and our systems indicate risk-on assets remain well-supported.

Our systems continue to indicate that growth & inflation remain elevated, and stocks and commodities are well-supported by our market regime signals. Our systems fared well during the last pandemic-induced correction; therefore, we expect them to perform similarly in the event of a variant-induced risk-off. For the time being, we think it is simply too early to make any significant risk management decisions. We are observing the situation and will update you on any changes in our systematic outlook as our models shift. Until next time!