Asset Allocation: Liquidity Views

Private Sector Dominant

Welcome to Prometheus Asset Allocation. The Prometheus Asset Allocation program offers a stable, macro-focused approach to asset management. Prometheus Asset Allocation aims to outperform a traditional stock and bond portfolio by leveraging our proprietary systematic macro process to rotate between 3 ETFs monthly (plus cash). As part of the program, we will be sharing our views on Growth, Inflation, and Liquidity in addition to our monthly video updates.

Our primary takeaways are as follows:

Liquidity is driven by both private and public sources. Currently, public sources face headwinds, whereas private sources remain dominant players in the liquidity ecosystem.

Reserve balances and commercial paper issuance remain neutral; bill issuance has slowed down but remains elevated; and repo activity remains extremely strong.

Overall, liquidity dynamics in the US remain stable, supporting all assets.

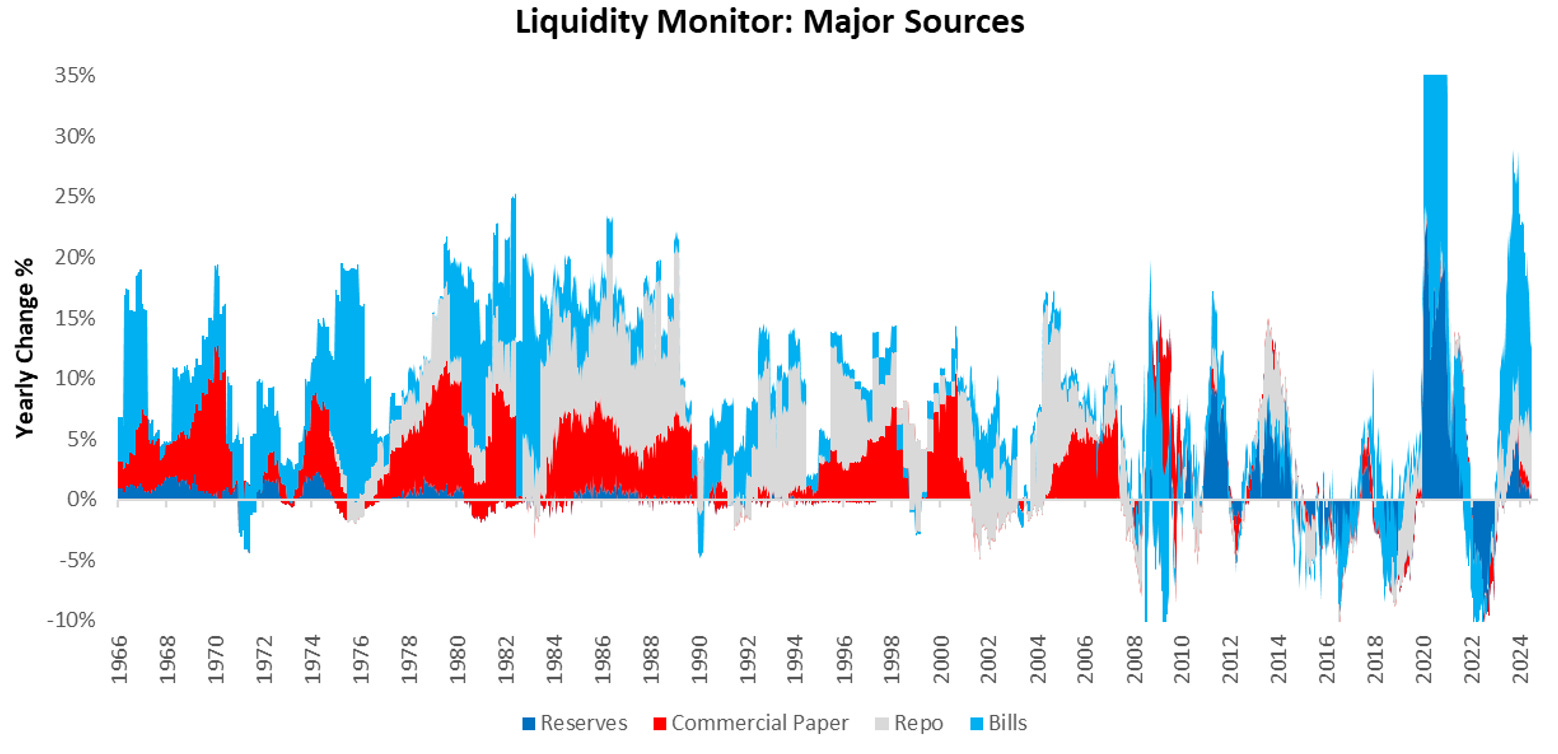

Liquidity is the flow of cash and cash-like assets that potentiate spending in the economy. Liquidity is determined by nominal dollar values and the relative risk profile of the various sources of liquidity. We begin our tracking of liquidity conditions by sharing the weighted growth rate of the major sources of liquidity: reserves, treasury bills, commercial paper, & repurchase agreements. As we can see below, the current liquidity dynamics are primarily driven by repo conditions after being dominated by treasury bill issuance.

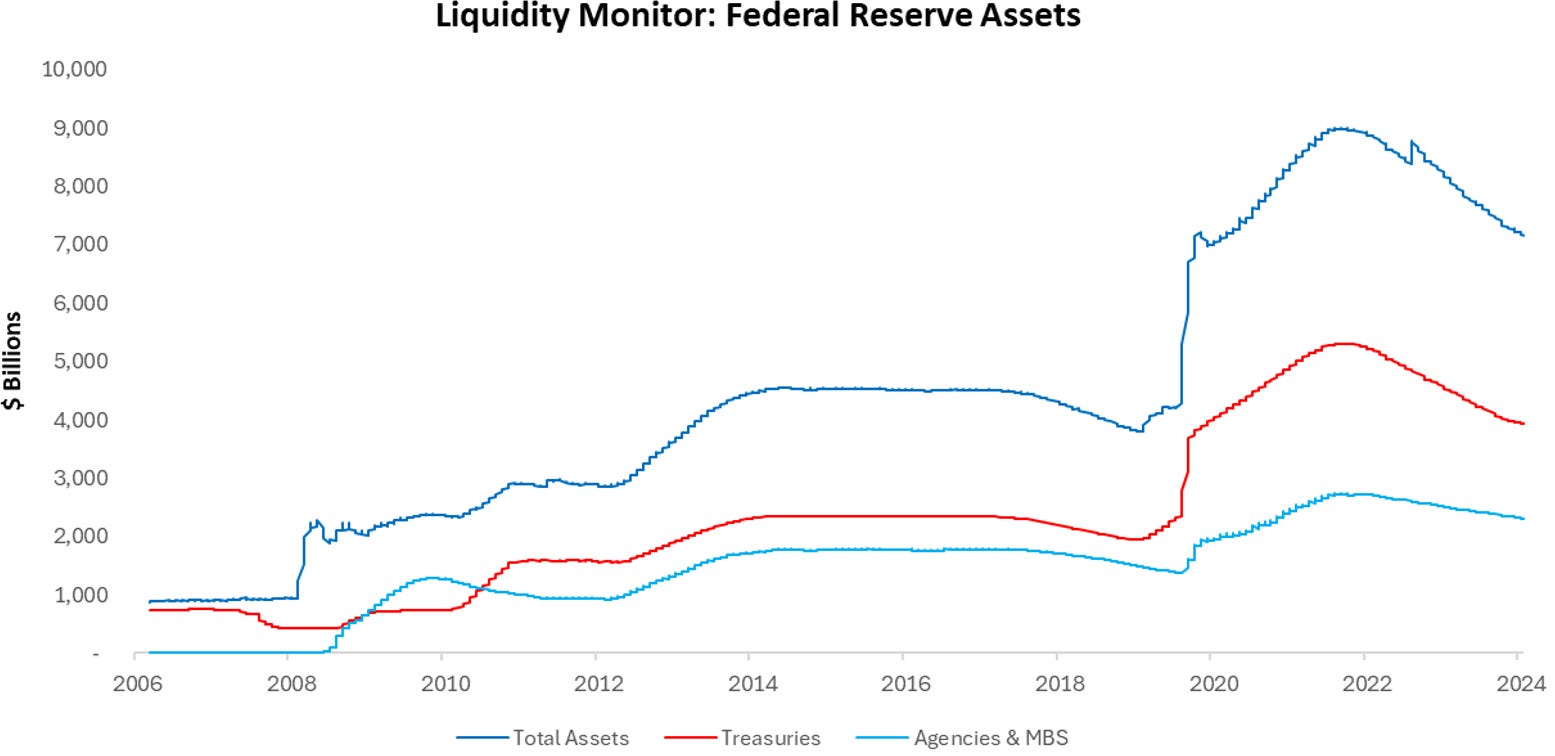

We zoom on each of these components, starting with reserve balances. Reserve balances held by financial institutions at the Fed are a function of the gross liquidity supplied by the Fed through the asset side of their balance sheet, relative to the gross liquidity absorbed by inflows into the liability side of their balance sheet. As we can see below, the current trend in reserve assets has been declining as the Fed engages in its QT program.

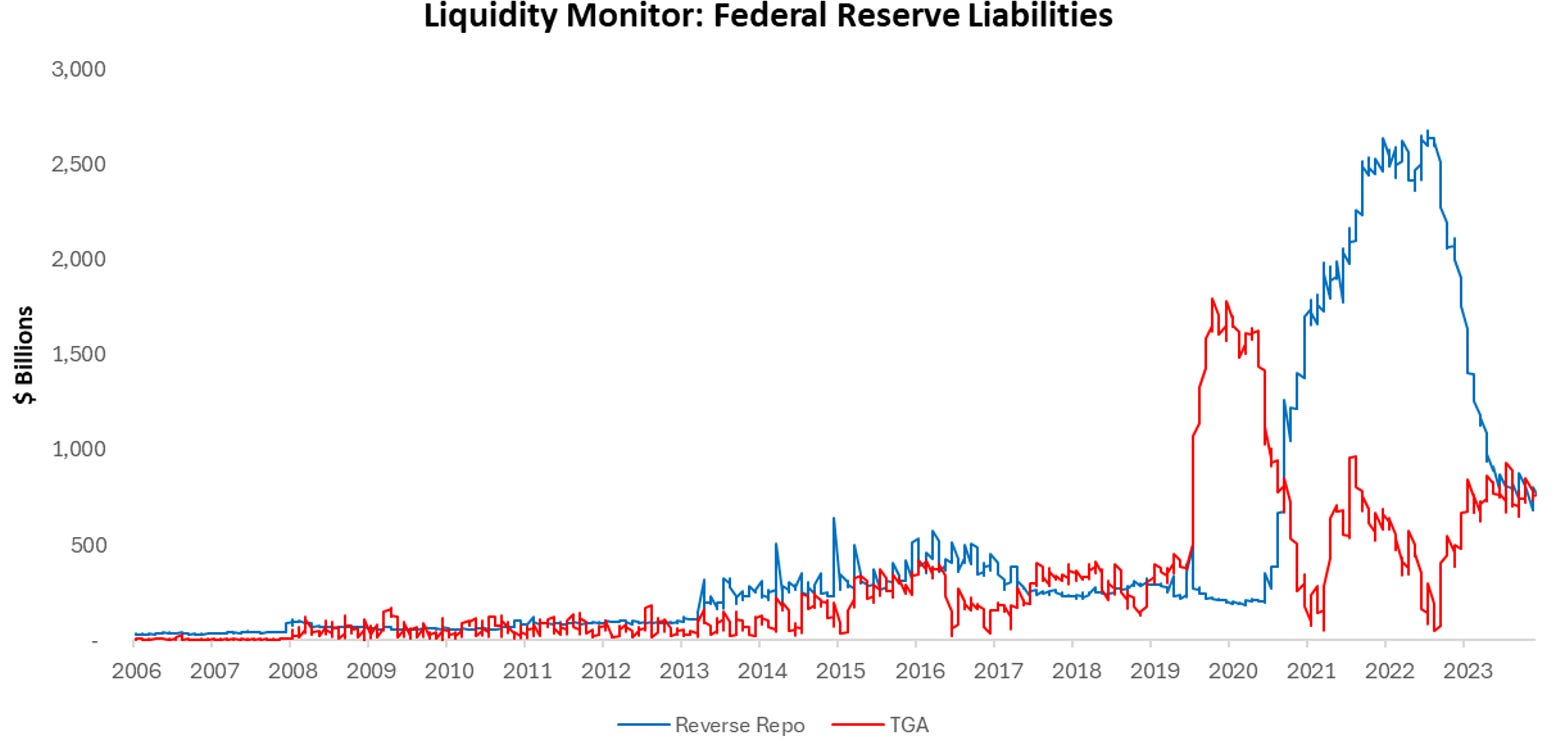

Next, examine the changes in major liabilities of the Fed, i.e. the liquidity drains on the financial sector. Note that, while the asset side is declining, the Fed liabilities, particularly the reverse repo are declining faster. Additionally, the trend in the TGA remains neutral. We visualize this below: